Digital Banking, Digital Wallet

Digital Wallet is a $10 Trillion Market: Here’s How to Profit From It

The convenience of paying for a product or service from a mobile or web wallet is nothing new. Digital wallets have been with us longer than you think. The technology was only subtly used. That was until the pandemic of 2020 exposed millions of people to the convenience digital wallets offer. And where people go, money follows.

The Digital Wallet Boom

Every booming technology had a predecessor or something that laid some foundation. For digital wallets, it was the rise of smartphones, e-commerce and contactless payments. By 2019, digital wallets have already gone mainstream, and 79% of consumers worldwide are now using contactless payments, especially in Europe and North America. While the market was huge even then, the business was controlled by a handful of brands like PayPal.

Fast-forward to 2020, when businesses were forced to operate online, and cash was hard to come by, digital wallets were quickly adopted as a payment solution. Today, it is regularly used by a broad cross-section of consumers in-store and online, fueling growth at an insanely fast pace.

How fast? In 2019, a report by eMarketer had that the number of people using digital wallets was expected to reach 2.1 billion by 2023, up from 1.6 billion that year. But just one year later, in 2020, digital wallet users surpassed that ‘expected’ number, towering to 2.8 billion users spending $5.5 trillion globally!

The number is expected to double in 2025 to 4.8 billion users spending $10 trillion worldwide.

Source: Payments Industry Intelligence | Mobile Wallet Users by 2025

Source: Payments Industry Intelligence | Mobile Wallet Users by 2025

Why Digital Wallets? You Ask — The Benefits

Convenience

One of the most significant advantages of digital wallets is their convenience. With a digital wallet, you can easily store and access all of your payment information in one place without carrying around multiple credit cards, debit cards, or cash. This not only makes it easier to make purchases, but it also reduces the risk of losing your cards or cash.

Security

Digital wallets also offer a high level of security. Most digital wallets use encryption technology to protect your payment information and may require you to authenticate your transactions with a fingerprint or other biometric data. This makes it much more difficult for fraudsters to access your payment information, which is particularly important when making online transactions.

Versatility

Another benefit of digital wallets is their versatility. Digital wallets can be used for various transactions, including online purchases, in-store purchases, and even peer-to-peer transactions. Many digital wallets also offer features such as loyalty programs and rewards, which can help you save money over time.

Cost effective

Compared to many payment methods, digital wallets are relatively cheaper. For example, sending money abroad through traditional methods can cost up to 10% of the transaction amount plus exchange rates. Also, transfer times can be long. By contrast, using a digital wallet to exchange currency, or pay someone in your network, can be instantaneous. And fees may be lower at less than 2%.

Similarly, investment firms usually transfer funds to and from their client’s bank accounts directly, but these transactions may take 2 to 5 business days. With a digital wallet such as PayPal, it could take only 1-2 working days to process at a 2.7% cost. Skrill offers the same service for just 1% within 1-7 days.

What are the Growth Drivers?

The rise of digital wallets can be attributed to several factors. Firstly, as more people use their smartphones for everyday activities, they would also use them to make payments.

Smartphones and mobile banking

Smartphones have been on the rise since the previous decade. With that rise comes mobile payment solutions like m-money and electronic money. In 2021 in Latin America, the use of smartphones jumped by 77% and is predicted to rise to 82% by 2025. This is significant as 70% of Latin Americans are either unbanked or underbanked, meaning that the reach of smartphones exceeds that of banking services.

Ahead of Latinos in Africa, with the most unbanked people using mobile payment solutions. Overall, 1.3 billion minors and 1.7 billion adults are underserved and unbanked globally.

Digital wallets loaded onto smartphones serve as a gateway to more advanced financial products for more people. They can empower individuals, economies, and societies by offering a convenient way to store digital value and make payments without cash.

Online transactions boom

Another factor driving the rise of digital wallets is the increasing number of online transactions. As more and more people are shopping online, digital wallets offer a secure and convenient way to make payments without entering your payment information every time.

Increasingly, customers want to purchase a wider range of products and services using their smartphones, not only at the point of sale but also throughout the entire discovery-to-decision journey. Storing value directly in a digital wallet on their phone makes this process much more convenient. This trend is predicted to continue growing in the future.

Adoption among young people

In addition, digital wallets are becoming increasingly popular with younger generations, who are more likely to use their smartphones for everyday activities. This demographic shift has led to a rise in digital wallets, as younger people are more likely to adopt new technologies and embrace new ways of handling their finances.

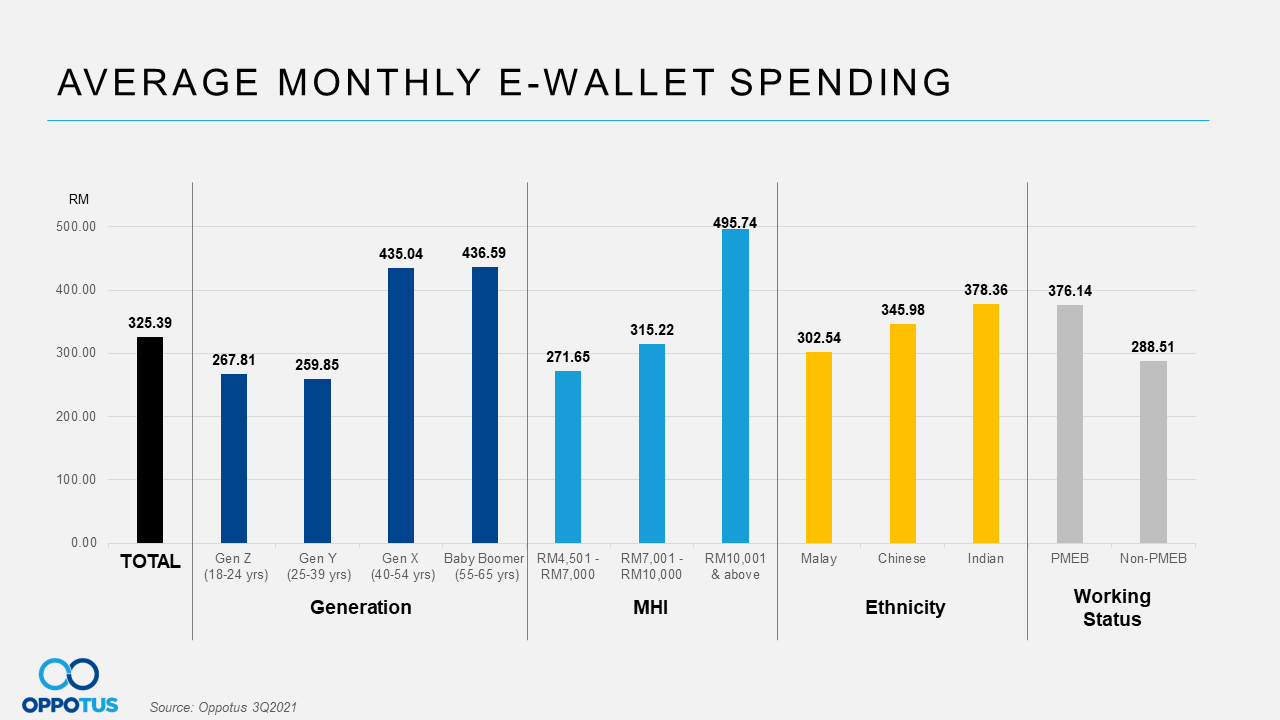

Here’s a 2021 report by Oppotus showing the average monthly e-wallet spending by Gen Z, Gen Y and Gen X in Malaysia.

Source: Oppotus 3Q2021

Digital Wallet isn’t Slowing Down

It’s clear that digital wallets are on the rise, but what does the future hold for this technology? One possibility is that digital wallets will become even more versatile and integrated into our daily lives. For example, digital wallets are used for everything from public transportation to vending machines.

Another possibility is that digital wallets will become even more secure as technology advances. Biometric authentication, such as facial and voice recognition, could become more widespread, making it even more difficult for fraudsters to access your payment information.

We could see digital wallets become even more popular with businesses as they offer a convenient and secure way to handle transactions. As more businesses adopt digital wallets, we could see a shift away from traditional payment methods, such as cash and checks.

Now we at the question, how do you profit from this $10 trillion potential market?

Accessing the ‘Wallet’ Opportunity

There’s a huge opportunity for savvy entrepreneurs or businesses looking to offer wallet solutions. Currently, there are 8 ways to tap into the market based on groups of digital wallet users:

- Instant Payouts: Offer instant payout wallets to gig economy workers like Bolt Drivers and freelancers. In Africa, instant payout wallets are booming, allowing Africans working for foreign employers to get paid in their local currencies on the spot.

- Payments and Check-outs: Online merchants rely on these wallets to let their customers store various cards, from debit cards to gift cards. This makes it easy for customers to make payments without including card information every time.

- Banking and unbanked: These wallets usually carry low KYC requirements giving access to finance to the unbanked and underserved customers.

- Super app: Superapp wallet solutions like Paytm offer more than seamless payments or digital-value storage. They are part of an ecosystem and can offer cashback. AmazonPay is another good example. A super app wallet is an excellent solution for building an ecosystem-like platform.

- Remittance: These wallets enable the storage, exchange and spending of multi-currencies. This is the ideal wallet solution for remittance, cross-border payments or forex businesses.

- Crypto wallets: Crypto wallets are relatively new, allowing the storage, spending, buying and selling of cryptocurrencies. These wallets can be made to accept fiat deposits and convert them into cryptos.

- Investments: These wallets are designed to let investors instantly collect proceeds from their investments (usually stock sales or bond returns). Etoro is a great example.

The access problem

While there is an opportunity, setting up a wallet solution or business requires a lot of consideration. First, you have to take the time to determine the need of target customers, your value proposition and how to monetise it.

Then you have to consider your capacity to deliver. A poorly implemented wallet solution will likely fail. Two groups of capacity questions to ask are:

- Internal technical resource:

- Do we understand the real cost of owning and maintaining a wallet infrastructure?

- Do we possess the technical capability necessary to build?

- Do we have the talent to sustain and assist with continuous improvements?

Business know-how

- Do we understand the market needs and the latest trends?

- Do we know what customers want from the solution we’re launching?

- Can we launch to market faster?

- What’s our buy model?

On average, it takes 12 months to build and launch a wallet solution if you’re building from scratch. The fastest has been 6 months. If you’re targeting a trending opportunity, time may be long before you launch.

The solution

Finslack Digital Wallet Solution allows you to build and launch your platform in weeks. We have built the infrastructure to start, scale and maintain digital wallet solutions, so you don’t have to. With 12 years of experience, we have partnered with leading compliance, BaaS and other service providers to ensure you launch to market with zero legal friction.

Finslack’s modular banking architecture, cloud-native infrastructure and customisable workflows offer the most flexibility to build and launch quickly.

Wrapping Up

With their convenience, security, and versatility, digital wallets offer a compelling alternative to traditional payment methods. Digital wallets and other forms of contactless payments will continue to be prevalent. Now more than ever is the opportunity to build the solution that will serve billions of customers, with Finslack helping you to profit faster.

3,961 Comments

Keep Reading...

Digital Banking, Digital Wallet, Payments November 15, 2023

The Exploding Digital Payment Economy in Nigeria and How Your Business Can Benefit From It

Digital payments have been around for a while in Nigeria.

e-commerce 2 years ago

Wow, amazing blog structure! How lengthy have you ever been running a blog for?

you make blogging glance easy. The overall look of your website is wonderful, as well as the content material!

You can see similar: dobry sklep

and here e-commerce

ecommerce 2 years ago

Hi there, You’ve done an excellent job. I’ll certainly digg it and

personally recommend to my friends. I am sure they’ll be benefited from

this web site. I saw similar here: ecommerce and also

here: ecommerce

Pillsvem 2 years ago

TruePills, No prescription needed, Buy pills without restrictions. Money Back Guaranteed 30-day refunds.

Trial ED Pack consists of the following ED drugs:

Viagra Active Ingredient: Sildenafil 100mg 5 pills

Cialis 20mg 5 pills

Levitra 20mg 5 pills

https://cutt.ly/7wC5m1Id

https://1c-kato.kg/bitrix/redirect.php?event1=&event2=&event3=&goto=https://true-pill.top/

https://garda-outlet.ru/bitrix/redirect.php?goto=https://true-pill.top/

https://monocle.p3k.io/preview?url=https%3A%2F%2Ftrue-pill.top

https://5.biqund.com/index/d2?diff=0&utm_source=ogdd&utm_campaign=26669&utm_content=&utm_clickid=l6o4wo4osowoss8w&aurl=https%3A%2F%2Ftrue-pill.top&an=&utm_term=&site=&isubs=0&pushMode=popup

https://softer.ru/bitrix/click.php?anything=here&goto=https://true-pill.top/

Cefdinirum

Briazide

Medicort

Pepsytoin

Plendil

Folister

Chemagyl

Carvedil

Proxatan

Valpakine

Allegra

Aluprex

Dramanyl

Azapin

Asacolon

Metrim

Nufapreg

Rheubalmin

Cyclo-progynova n

Nidagel

Painflex

Latrigin

Meclizine

Spersanicol

Noraxin

Meksun

Isotret

Lorita

Ivenox

Bio-atenolol

Pristiq

Calcigard

Aldonar

Releve

Reclomide

Oestro

Ermac

Teroxina

Terazon

Sedoran

sklep internetowy 2 years ago

Hello, Neat post. There’s a problem along with your website in internet explorer, would test this?

IE still is the market leader and a huge

portion of folks will miss your fantastic writing due to this problem.

I saw similar here: Sklep internetowy

sklep internetowy 2 years ago

Good day! I could have sworn I’ve visited this web site before but after looking at many

of the articles I realized it’s new to me. Regardless, I’m

certainly pleased I came across it and I’ll be bookmarking

it and checking back often! I saw similar here: Ecommerce

Quilicarbor 2 years ago

Сериал про космос – сериал звездные врата смотеть онлайн

Mike Morgan 2 years ago

Howdy

I have just analyzed finslack.com for its SEO metrics and saw that your website could use a boost.

We will improve your ranks organically and safely, using only state of the art AI and whitehat methods, while providing monthly reports and outstanding support.

More info:

https://www.digital-x-press.com/unbeatable-seo/

Regards

Mike Morgan

Digital X SEO Experts

e-commerce 2 years ago

Hello there! Do you know if they make any plugins to help with Search Engine Optimization? I’m trying to get my

blog to rank for some targeted keywords but I’m

not seeing very good gains. If you know of any please share.

Thank you! You can read similar text here: Dobry sklep

Analytical and Research Agency 2 years ago

It’s very interesting! If you need help, look here: ARA Agency

Mike Mackenzie 2 years ago

Good Day

This is Mike Mackenzie

Let me introduce to you our latest research results from our constant SEO feedbacks that we have from our plans:

https://www.strictlydigital.net/product/semrush-backlinks/

The new Semrush Backlinks, which will make your finslack.com SEO trend have an immediate push.

The method is actually very simple, we are building links from domains that have a high number of keywords ranking for them.

Forget about the SEO metrics or any other factors that so many tools try to teach you that is good. The most valuable link is the one that comes from a website that has a healthy trend and lots of ranking keywords.

We thought about that, so we have built this plan for you

Check in detail here:

https://www.strictlydigital.net/product/semrush-backlinks/

Cheap and effective

Try it anytime soon

Regards

Mike Mackenzie

mike@strictlydigital.net

zakaz-kuhni-cena-CalvinidowL 2 years ago

купить сумку на колесах в интернет магазине недорого в москве

http://google.hu/url?q=http://dorozhnye-sumki-kolesa.ru

hitman.agency 2 years ago

Hello! Do you know if they make any plugins to assist with SEO?

I’m trying to get my site to rank for some targeted keywords but I’m not seeing very good

success. If you know of any please share. Kudos! I saw similar art here: Hitman.agency

Mike Chesterton 2 years ago

Hi there,

I have reviewed your domain in MOZ and have observed that you may benefit from an increase in authority.

Our solution guarantees you a high-quality domain authority score within a period of three months. This will increase your organic visibility and strengthen your website authority, thus making it stronger against Google updates.

Check out our deals for more details.

https://www.monkeydigital.co/domain-authority-plan/

NEW: Ahrefs Domain Rating

https://www.monkeydigital.co/ahrefs-seo/

Thanks and regards

Mike Chesterton

Mike Jeff 2 years ago

This service is perfect for boosting your local business’ visibility on the map in a specific location.

We provide Google Maps listing management, optimization, and promotion services that cover everything needed to rank in the Google 3-Pack.

More info:

https://www.speed-seo.net/ranking-in-the-maps-means-sales/

Thanks and Regards

Mike Jeff

PS: Want a ONE-TIME comprehensive local plan that covers everything?

https://www.speed-seo.net/product/local-seo-bundle/

Mike Wallace 2 years ago

Hi there

Just checked your finslack.com baclink profile, I noticed a moderate percentage of toxic links pointing to your website

We will investigate each link for its toxicity and perform a professional clean up for you free of charge.

Start recovering your ranks today:

https://www.hilkom-digital.de/professional-linksprofile-clean-up-service/

Regards

Mike Wallace

Hilkom Digital SEO Experts

https://www.hilkom-digital.de/

buy valtrex 500 mg 2 years ago

valtrex online australia

cheapest prednisone no prescription 2 years ago

prednisone 5

RichardClica 2 years ago

Миотокс в ботулинотерапии: секрет успешных процедур

миотокс препарат цена отзывы по применению http://www.miotoks.ru .

prednisone tablets 5mg price 2 years ago

no prescription prednisone

generic zithromax over the counter 2 years ago

azithromycin buy online india

synthroid 37 mcg 2 years ago

synthroid 62.5 mcg

buying valtrex online 2 years ago

valtrex capsules

Mike Taylor 2 years ago

Good Day

I have just took a look on your SEO for finslack.com for the current search visibility and saw that your website could use a push.

We will enhance your ranks organically and safely, using only state of the art AI and whitehat methods, while providing monthly reports and outstanding support.

More info:

https://www.digital-x-press.com/unbeatable-seo/

Regards

Mike Taylor

Digital X SEO Experts

Filomena05 2 years ago

Wow, superb weblog structure!

How long have you been blogging for? you make running

a blog look easy. The whole glance of your website is magnificent, let alone the

content material! I saw similar here prev next and that was wrote by Arron70.

Mike Mercer 2 years ago

Hello

This is Mike Mercer

Let me present you our latest research results from our constant SEO feedbacks that we have from our plans:

https://www.strictlydigital.net/product/semrush-backlinks/

The new Semrush Backlinks, which will make your finslack.com SEO trend have an immediate push.

The method is actually very simple, we are building links from domains that have a high number of keywords ranking for them.

Forget about the SEO metrics or any other factors that so many tools try to teach you that is good. The most valuable link is the one that comes from a website that has a healthy trend and lots of ranking keywords.

We thought about that, so we have built this plan for you

Check in detail here:

https://www.strictlydigital.net/product/semrush-backlinks/

Cheap and effective

Try it anytime soon

Regards

Mike Mercer

mike@strictlydigital.net

Pillsvem 2 years ago

Erectile dysfunction treatments available online from TruePills.

Discreet, next day delivery and lowest price guarantee.

Viagra is a well-known, branded and common erectile dysfunction (ED) treatment for men.

It’s available through our Online TruePills service.

Trial ED Pack consists of the following ED drugs:

Viagra Active Ingredient: Sildenafil 100mg 5 pills

Cialis 20mg 5 pills

Levitra 20mg 5 pills

https://cutt.ly/dw7ChH4s

https://dulevo-repair.ru/bitrix/redirect.php?goto=https://true-pill.top/

https://m.en.acmedelavie.com/member/login.html?returnUrl=https://true-pill.top/

https://optic-street.ru/bitrix/redirect.php?goto=https://true-pill.top/

https://hiroko-ny.hatenadiary.com/iframe/hatena_bookmark_comment?canonical_uri=https://true-pill.top/

http://maxlit.ru/bitrix/redirect.php?goto=https://true-pill.top/

Fortzaar

Herpesnil

Mediolax

Deflamon

Flavonate

Neopramiel

Fusix

Ketoskin

Dexafrin

Geratam

Unipril

Denitine

Aravida

Rivastigmine

Prazolo

Azimex

Cleocin

Febrax

Timox

Tizem

Bi-euglucon m

Adenosan

Isoniazidum

Gynokadin

Lansoprazola

Cipril

Femixol

Omeprazol

Zestaval

Allopur

Votum plus

Denulcer

Prasocid

Zandid

Indomen

Hoggar

Ifitrim

Socalm

Eskalit

Sharizol

canadian pharmacy 5 mg prednisone no rx 2 years ago

buy prednisone online canada

how to get valtrex online 2 years ago

valtrex 1000 mg tablet

Mike Donaldson 2 years ago

Hi there,

I have reviewed your domain in MOZ and have observed that you may benefit from an increase in authority.

Our solution guarantees you a high-quality domain authority score within a period of three months. This will increase your organic visibility and strengthen your website authority, thus making it stronger against Google updates.

Check out our deals for more details.

https://www.monkeydigital.co/domain-authority-plan/

NEW: Ahrefs Domain Rating

https://www.monkeydigital.co/ahrefs-seo/

Thanks and regards

Mike Donaldson

Mike Benson 2 years ago

This service is perfect for boosting your local business’ visibility on the map in a specific location.

We provide Google Maps listing management, optimization, and promotion services that cover everything needed to rank in the Google 3-Pack.

More info:

https://www.speed-seo.net/ranking-in-the-maps-means-sales/

Thanks and Regards

Mike Benson

PS: Want a ONE-TIME comprehensive local plan that covers everything?

https://www.speed-seo.net/product/local-seo-bundle/

Mike Davidson 2 years ago

Hi there,

My name is Mike from Monkey Digital,

Allow me to present to you a lifetime revenue opportunity of 35%

That’s right, you can earn 35% of every order made by your affiliate for life.

Simply register with us, generate your affiliate links, and incorporate them on your website, and you are done. It takes only 5 minutes to set up everything, and the payouts are sent each month.

Click here to enroll with us today:

https://www.monkeydigital.org/affiliate-dashboard/

Think about it,

Every website owner requires the use of search engine optimization (SEO) for their website. This endeavor holds significant potential for both parties involved.

Thanks and regards

Mike Davidson

Monkey Digital

azithromycin medication 2 years ago

azithromycin 4 pills

Raymondunfip 2 years ago

Howdy-ho! finslack.com

Did you know that it is possible to send appeals authorizedly? We suggest a new, unique method of sending appeals through contact forms.

Messages sent through Contact Forms are usually seen as important, so they don’t normally end up in spam.

Trу out our service without paying a dіme!

We can send out up to 50,000 messages for you.

The cost of sending one million messages is $59.

This message was automatically generated.

Please use the contact details below to get in touch with us.

Contact us.

Telegram – https://t.me/FeedbackFormEU

Skype live:feedbackform2019

WhatsApp +375259112693

WhatsApp https://wa.me/+375259112693

We only use chat for communication.

Mike Richards 2 years ago

Hi there

Just checked your finslack.com baclink profile, I noticed a moderate percentage of toxic links pointing to your website

We will investigate each link for its toxicity and perform a professional clean up for you free of charge.

Start recovering your ranks today:

https://www.hilkom-digital.de/professional-linksprofile-clean-up-service/

Regards

Mike Richards

Hilkom Digital SEO Experts

https://www.hilkom-digital.de/

synthroid levothyroxine 2 years ago

synthroid 0.0125 mcg

Zobacz jak 2 years ago

great article

purchase 2 years ago

doxycycline canada

prescription 2 years ago

30 furosemide 20 mg

NikeBug 2 years ago

darkmarket link https://mydarkmarket.com/ – deep web links dark web links

NikeBug 2 years ago

bitcoin dark web https://mydarkmarket.com/ – darknet market lists darkmarkets

mozglike 2 years ago

Ad disputandum — Для обсуждения.

mozgyou 2 years ago

Contradictio in re — лог. Противоречие в существе (нелепость).

Mike Warren 2 years ago

Hi there

I have just analyzed finslack.com for the ranking keywords and saw that your website could use a push.

We will improve your ranks organically and safely, using only state of the art AI and whitehat methods, while providing monthly reports and outstanding support.

More info:

https://www.digital-x-press.com/unbeatable-seo/

Regards

Mike Warren

Digital X SEO Experts

NikeBug 2 years ago

dark web markets https://mydarknetmarketlinks.com/ – dark websites darknet sites

NikeBug 2 years ago

dark web sites links https://mydarknetmarketlinks.com/ – dark web links darknet market

NikeBug 2 years ago

dark market url https://mydarknetmarketlinks.com/ – the dark internet darkmarket link

zithromax 250 capsules 2 years ago

azithromycin without prescription

NikeBug 2 years ago

dark web markets https://mydarknetmarketlinks.com/ – darkmarkets tor market

NikeBug 2 years ago

darknet drug market https://mydarknetmarketlinks.com/ – dark markets deep web drug links

NLP 2 years ago

Мури С., Грир С. и популярные обзоры по психологии.

smotretq 2 years ago

Veni, vidi, vici

kinop 2 years ago

Dictum – factum

smotretc 2 years ago

100 лет тому вперед смотреть фильм. 100 лет тому вперед 1080.

smotretz 2 years ago

100 лет тому вперед смотреть фильм онлайн. 100 лет тому вперед 2024 смотреть онлайн.

azithromycin price in usa 2 years ago

azithromycin price

filmd 2 years ago

100 лет тому вперед фильм смотреть бесплатно. 100 лет тому вперед фильм 2024 смотреть.

Verzaima 2 years ago

В нашем Telegram-канале вы найдете самые свежие и проверенные предложения от новых МФО. Мы ежедневно обновляем информацию, чтобы вы могли выбрать лучшие условия. Если вам срочно нужны деньги, мы расскажем вам про новый займ на карту без отказа. Получить деньги теперь можно даже при плохой кредитной истории. Наш канал поможет вам найти самый выгодный и надежный вариант. Подписывайтесь и узнайте больше о новых МФО!

online 2 years ago

ciprofloxacin capsule

onlined 2 years ago

Уэнздей 1 сезон 2024

Fmoshkahop 2 years ago

Я всегда мечтал посетить Париж. Когда подвернулся выгодный тур, у меня не было достаточно средств. Но благодаря телеграм-каналу МФО 2024 на карту онлайн я быстро нашел займ и осуществил свою мечту. Путешествие в Париж стало незабываемым и оставило массу ярких впечатлений.

smotretf 2 years ago

Фоллаут 1 сезон смотреть онлайн

kinoc 2 years ago

Король и шут 1 сезон смотреть онлайн

Richardwet 2 years ago

ремонт сотовых

Howardneome 2 years ago

https://vyzvat-taksi.ru/

Kak_atKa 2 years ago

Легко и быстро избавьтесь от бородавок в домашних условиях.

Лекарство от бородавок http://www.plastica.onclinic.ru .

TumerNethy 2 years ago

Hello.

This post was created with 2ssdsd3222aa.com

AlbertoErund 2 years ago

заказать интернет рекламу

onlineh 2 years ago

Главвный герой 2024

vse mfo 2 years ago

Ищете надежный способ получить деньги без отказа? Добро пожаловать в телеграм-канал какой займ можно взять без проблем на карту ! У нас собраны МФО, которые дают деньги без проверки кредитной истории. Первый займ под 0% до 15 000 рублей за 10 минут! В канале представлены новые МФО 2024 года, которые выдают мгновенные микрозаймы даже при плохой кредитной истории и просрочках. Подпишитесь и получайте деньги без проблем и ожиданий!

VisboeMub 2 years ago

Наш Бош центр в Москве предлагает лучшие условия для ремонта бытовой техники. Бесплатная диагностика, ремонт на дому и гарантия на 1 год — все это обеспечивает высокий уровень сервиса и удовлетворение клиентов.Доверьте свою технику профессионалам! Наш сервисный центр Бош с более чем 10-летним опытом предлагает качественное обслуживание и ремонт бытовых приборов. Мы используем оригинальные запчасти и предоставляем бесплатный выезд мастера для диагностики и ремонта.

Julia Schneider 2 years ago

Du hast auch einen Impfschaden oder Nebenwirkungen nach der Corona-Impfung?

Ich leite dir diese Nachricht vom Verein BÜRGERSCHUTZ weiter, weil ich gehört habe, dass du und einige deiner Freunde Impfnebenwirkungen habt oder befürchtet, welche zu bekommen. Als Geimpfte könnten wir jetzt 6.000 € Schadenersatz vom Impfarzt erhalten.

Der Verein Bürgerschutz, Österreichs größter „Impfopfer-Verein“, unterstützt dich bei Impfschäden nach deiner mRNA-Behandlung oder IMPFAUSLEITUNG.

Zusätzlich erhalten alle Mitglieder vom https://www.buergerschutz.org kostenlos eine Anleitung zur Impfausleitung.

Leite diese Nachricht weiter, um den Druck auf die Impfärzte und die Regierung zu erhöhen.

LG

Julia

Partnerprogramm Wohncontainer

https://skycontainer.at/

Bertakiimmit 2 years ago

Моему автомобилю срочно потребовался ремонт, а нужной суммы в 10 тысяч рублей под рукой не оказалось. Обратившись за помощью к друзьям, я узнал о канале https://t.me/s/novue_zaimu, где можно было найти множество новых займов онлайн. Благодаря полезной информации о том, как правильно заполнять заявки, я получил деньги на ремонт автомобиля уже на следующий день. Ремонт был сделан вовремя, и я снова мог пользоваться своим автомобилем.

tablets 2 years ago

tamoxifen 5648

cheap 2 years ago

flomax erectile dysfunction

kinoa 2 years ago

Претенденты смотреть Претенденты фильм, 2024, смотреть онлайн

enkokeype 2 years ago

Портал uafakty.com.ua его пользователи отмечают лаконичность оформления. Здесь затрагиваются темы культуры, политики, спорта. Вас ждут интересные новости шоу-бизнеса. Наслаждайтесь достойным контентом! uafakty.com.ua – https://uafakty.com.ua портал, который ценится за объективность и оперативность, он вам будет понятен. Тут имеется много полезной информации, ознакомиться с ней можно в любое удобное время. Все статьи удобны для чтения и снабжены фотографиями. Заходите на наш популярный сайт и читайте актуальные новости в любое время!

Vkaromop 2 years ago

Поменять холодное остекление на теплое спб specbalkon.ru

Организация СПЕЦ Балкон предлагает услуги по замене остекления, утеплению и ремонту балконов в Спб. Мы специализируемся именно на балконах, что дает возможность сосредоточиться на надежности и скорости работы. При оформлении заказа на сайте specbalkon.ru остекления и отделки «под ключ» мы дарим скидку в 10 %. Прямо сейчас переходите на наш веб ресурс и оставляйте заявку.

Если Вам требуется поменять холодное остекление на теплое прямо сейчас, то мы вам обязательно окажем помощь. Услуга по замене холодного фасадного остекления по теплое в данный момент весьма востребована. При покупке жилья в новом доме очень часто застройщик ставит на балкон холодное, не очень хорошее остекление, которое лучше всего менять сразу же после покупки. Теплое остекление лоджии имеет большое количество плюсов: окна не замерзают даже в самые морозные зимы, на балконе возможно сделать любое помещение, цветы будут стоять при комфортной температуре, на балконе можно сделать места для хранения и вещи не деформируются. Поэтому предлагаем Вам замену остекления сделать как можно скорее и по выгодной цене.

По поводу крыша над балконом недорого, обращайтесь к нам. Контактный номер телефона +7(812)240-94-42 или закажите обратный звонок на вышеуказанном сайте. Мы осуществляем монтаж в точно установленный срок, обычно в течение 1-3 дней. Даётся гарантия на материалы в среднем 5 лет, на работу — 3 года. Оплата осуществляется по факту выполненных работ, предоплата не потребуется.

Фирма specbalkon.ru расположена по адресу: Санкт-Петербург, ул. Оптиков, д. 4. Режим работы с пн по вс с 10:00 до 19:00. Также мы делаем крыши на балконы с установкой, внешнюю отделку парапета, внутреннюю отделку балкона по вашему дизайну. Звоните, приходите, будем рады с Вами сотрудничать.

MichaelGap 2 years ago

излечение от алкоголизма https://medutox.ru/

ninadacicy 2 years ago

Portál szakemberek keresőjének https://szakiweb.hu/ -Látogass el az oldalra és találsz egy mesterembert építkezésre, javításra, ház körüli segítségre. Nagyon könnyű mestert vagy szakembert találni az országban bárhol. Vegye igénybe az oldalon található szakemberek szolgáltatásait.

ekahuAmato 2 years ago

Вывоз мусора на утилизацию в Москве https://vyvoz.pro/ по лучшей цене. Постоянно на линии более 50 машин разной вместимости. Узнайте на сайте все наши услуги по утилизации, а мы приедем быстро, в течении 30 минут. Вы можете написать нам в чат на сайте или просто позвонить по телефону. Максимально быстро приедем. Заказать вывоз мусора от профессионалов у нас на сайте.

Rustesap 2 years ago

Вас интересует профессиональный ремонт электро-транспорта в Минске? Мастерская 911 – это то, что вам нужно! В сервисном центре трудятся самые лучшие специалисты, которые имеют достаточный опыт работы. Они великолепно разбираются в электросамокатах, качественно и оперативно их ремонтируют. https://m911.by/ – сайт, где можете в любое удобное время ознакомиться с нашими услугами. Мы обеспечиваем своих клиентов недорогим ремонтом любого вида электро-транспорта. Обращайтесь именно к нам, продиагностируем поломку абсолютно бесплатно.

Basilhtup 2 years ago

На сайте https://cliningkrd.ru вы сможете заказать обратный звонок для того, чтобы воспользоваться услугами клининговой компании «Cleaning». Здесь оказываются профессиональные услуги компетентными, проверенными специалистами. В работе применяется инновационное, высокотехнологичное оборудование, которое справляется с загрязнениями различного уровня интенсивности. Бытовая химия, чистящие средства от надежных брендов, которые создают полностью безопасную для людей, животных продукцию.

etmanhible 2 years ago

Space Movers https://spacemovers.ca/ is renowned as the premier moving company in Calgary, Canada, offering unparalleled service and expertise in residential and commercial relocations. Their reputation as the best movers in the city is built on a foundation of reliability, efficiency, and a customer-centric approach that ensures a smooth and stress-free moving experience. Choosing Space Movers means choosing the best in the business, ensuring a seamless transition to your new home or office.

website 2 years ago

Your passion for the subject matter is evident in every post you write. This was another outstanding article. Thank you for sharing!coinsslot

Vaifroxejoivy 2 years ago

Аттестация медработников на повышение maps-edu.ru

Онлайн обучение сейчас с каждым днем оказывается только популярнее. Это комфортно, недолго и недорого, при том, что информативность обучения не теряется и Вы получаете государственные документы после завершения. Академия «МАПС» рассказывает о своих программах на веб портале maps-edu.ru и поможет с выбором программы, нужной именно Вам.

Что касается курсы логопеда дистанционное обучение с сертификатом цена – Вы на верном пути. Направления, по которым мы обучаем: строительство, агрономия и сельское хозяйство, педагогика, физическая культура и спорт, пожарная безопасность, закупки, культура и искусство, промышленность, нефтяная и газовая промышленность, метрология и стандартизация и многие другие. Со студентами оформляем договор и работаем по его плану. Имеем все запрашиваемые лицензии на обучающую деятельность, а по итогу все документы заносятся в ФИС ФРДО. У нас уже много выпускников окончили обучение и написали отзывы, прочтите их обязательно на указанном интернет портале.

Особенно хочется выделить набор услуг для медицинских работников. Это аккредитация, профессиональная переподготовка, набор баллов НМО, обучение среднего медперсонала и другие. Указанная категория весьма популярна, поскольку медицина в нашей стране прогрессирует ежедневно. Чтобы быть в курсе всех новых методов лечения, лекарств, аппаратов, врачам нужно постоянно проходить обучение. А способ удаленно подходит всем без исключения. Удобно и выгодно в наше нелегкое время.

По теме профессиональная переподготовка педагогика онлайн, мы Вам обязательно поможем. Звоните по телефону 8(800)777-06-74 и задавайте все оставшиеся вопросы. Звонок по России бесплатный. Регионально расположены по адресу: г. Иркутск, ул. Степана Разина, д. 6. На веб портале maps-edu.ru вы также сможете обратиться в службу поддержки и Вас проконсультирует наш менеджер.

MarcusCrato 2 years ago

выкуп авто москва быстро выкуп любого авто

ThomasFup 2 years ago

have a peek at these guys best solana wallet

Chrisviolo 2 years ago

visit the site sollet wallet login

Georgerex 2 years ago

this https://blur-io-nft.com/2023/11/09/how-the-blur-nft-blend-is-changing-the-perception-of-digital-art/

Cesarmox 2 years ago

Homepage https://kombonovaya5.com/

Lloydtrose 2 years ago

Get the facts https://galxe-app.org/2023/11/19/galxe-protocol-revolutionizing-existing-systems-and-creating-new-opportunities-for-users/

Jacobalank 2 years ago

you can try this out https://galxe-web3.com/2023/11/19/galxe-introduces-new-feature-to-empower-users-and-enhance-web3-experience/

JamesthEde 2 years ago

https://fraza.kyiv.ua/ вы найдете последние новости, глубокие аналитические материалы, интервью с влиятельными личностями и экспертные мнения. Следите за важными событиями и трендами в реальном времени. Присоединяйтесь к нашему сообществу и будьте информированы!

MapEdu 2 years ago

Сколько стоит аккредитация онлайн maps-edu.ru

По теме переподготовка специалист по охране труда дистанционно онлайн, мы Вам обязательно поможем. Звоните по контактному телефону 8(800)777-06-74 и задавайте все оставшиеся вопросы. Звонок по РФ бесплатный. Регионально расположены по адресу: г. Иркутск, ул. Степана Разина, д. 6. На сайте maps-edu.ru вы также можете обратиться в службу поддержки и Вас проконсультирует наш специалист.

Antonioobene 2 years ago

купить куклу в секс шопе https://24sexy-dolls.ru

Arthurlon 2 years ago

https://7krasotok.com здесь вы найдете статьи о моде, красоте, здоровье, отношениях и карьере. Читайте советы экспертов, участвуйте в обсуждениях и вдохновляйтесь новыми идеями. Присоединяйтесь к нашему сообществу женщин, стремящихся к совершенству!

Darrylbrawn 2 years ago

https://bestwoman.kyiv.ua узнайте всё о моде, красоте, здоровье и личностном росте. Читайте вдохновляющие истории, экспертные советы и актуальные новости. Присоединяйтесь к нашему сообществу женщин, живущих яркой и насыщенной жизнью!

MatthewVut 2 years ago

https://prowoman.kyiv.ua на нашем сайте вы найдете полезные советы по моде, красоте, здоровью и отношениям. Читайте вдохновляющие статьи, участвуйте в обсуждениях и обменивайтесь идеями. Присоединяйтесь к нашему сообществу современных женщин!

Thomassoymn 2 years ago

https://superwoman.kyiv.ua вы на нашем надежном гиде в мире женской красоты и стиля жизни! У нас вы найдете актуальные статьи о моде, красоте, здоровье, а также советы по саморазвитию и карьерному росту. Присоединяйтесь к нам и обретайте новые знания и вдохновение каждый день!

Byronneulk 2 years ago

buy tiktok views live Buy TikTok Live Views

GlennJog 2 years ago

курсовые на заказ https://kursovyematematika.ru

RobertDup 2 years ago

решения задач на заказ https://resheniezadachmatematika.ru/

DavidWreni 2 years ago

Сайт https://zhenskiy.kyiv.ua – це онлайн-ресурс, який присвячений жіночим темам та інтересам. Тут зібрана інформація про моду, красу, здоров’я, відносини, кулінарію та багато іншого, що може бути корисним та цікавим для сучасних жінок.

Lervaenum 2 years ago

Не знаете, где взять деньги срочно? Наш канал срочные займы предлагает самые надежные и проверенные МФО. Займы на карту без отказа, быстро и удобно. Подписывайтесь и будьте в курсе всех выгодных предложений!

BrandonMeame 2 years ago

Доставка цветов в Саратове https://flowers64.ru/ это отличная возможность заказать различные цветы, букеты, композиции, подарки, не выходя из дома.

JamesWam 2 years ago

заказать курсовую работу https://kupit-kursovuyu-rabotu.ru/ с гарантией и антиплагиатом

rooftop ac unit installation 2 years ago

There’s noticeably a bundle to find out about this. I assume you made sure nice points in options also.

commercial aircon installation 2 years ago

At this time it looks like WordPress is the preferred blogging platform available right now. (from what I’ve read) Is that what you’re using on your blog?

Arturoblosy 2 years ago

Больше интересной информации о строительстве и ремонте можно прочитать на сайте https://stroyka-gid.ru. Только самые популярные статьи и обзоры процесса ремонта помещений и строительства зданий.

domestic air conditioning installation 2 years ago

First Of All, let me commend your clearness on this subject. I am not an expert on this topic, but after registering your article, my understanding has developed well. Please permit me to take hold of your rss feed to stay in touch with any potential updates. Solid job and will pass it on to supporters and my online readers.

HenryNit 2 years ago

first reseller panel first reseller panel

Timothyfex 2 years ago

instagram promotion services https://promobanger.com/

Shawnfleby 2 years ago

music promotion packages free music promotion

pharmacy 2 years ago

provigil over the counter

DavidBar 2 years ago

курсовые работы на заказ https://zakazat-kursovuyu-rabotu7.ru

JeffreyCat 2 years ago

такси город горячая линия такси

DarrellJoumn 2 years ago

такси бизнес класс дешевое такси

ShawnRoyak 2 years ago

сколько стоит такси https://taxi-vyzvat.ru

MiguelLic 2 years ago

Доставка цветов в Саратове https://www.expressbuket24.ru/ это отличная возможность заказать различные цветы, букеты, композиции, подарки, не выходя из дома. Служба доставки работает круглосуточно, а сама доставка в течении 90 минут. Вы сможете подарить букет анонимно, просто напишите это при заказе. Огромный ассортимент цветов порадует всех!

KevinKam 2 years ago

курсовые работы на заказ https://zakazat-kontrolnuyu7.ru

Richardkag 2 years ago

решение задач на заказ https://resheniye-zadach7.ru заказать онлайн

EdwardModay 2 years ago

рефераты на заказ https://kupit-referat213.ru

GeraldPef 2 years ago

https://bicrypto.exchange – crypto exchange software. White label, open-source exchange solution with a focus on a super-fast, pixel-perfect interface and robust security. High-performance platform with a robust internal architecture. Leverages the capabilities of Nuxt3 to create a cutting-edge user interface.

Jerrytop 2 years ago

анаденантера иноземная купить кратом купить

Sdelat_dsSr 2 years ago

Как сделать качественную шумоизоляцию в автомобиле в Москве?

Услуги шумоизоляции автомобиля цена https://shumoizolyaciya-a.ru .

JamesAgeby 2 years ago

купить диплом юриста

посмотреть сайт

JamesEluck 2 years ago

купить диплом в нижнем новгороде

на сайте

WilliamHeshy 2 years ago

купить диплом старого образца https://www.6landik-diploms.com

Michaelvow 2 years ago

twin casino регистрация Twin Casino

JosephSlorn 2 years ago

акриловый сайдинг купить сайдинг для дома

Alvarofaw 2 years ago

sites Best cc+cvv

Thomaslup 2 years ago

straight from the source Bank cards

Geraldfausa 2 years ago

производство сыровяленых деликатесов мясо прошутто

JamesDib 2 years ago

Все самое интересное из мира игр https://unionbattle.ru обзоры, статьи и ответы на вопросы

Martinrew 2 years ago

купить квартиру недорого https://kupit-kvartiruekb.ru

BneryuaUnada 2 years ago

My girlfriend and I were looking for some fun adult entertainment, and we turned to Google for help. That’s how we discovered Mult34 – steven universe porn . We spent the entire evening exploring the site, enjoying a vast selection of erotic comics.

The content on Mult34 – rick and morty porn is impressive, with a variety of stories that kept us entertained all night. If you’re looking for quality adult comics, this site is a must-visit. We had a fantastic time and will definitely be coming back to Mult34 – starfire porn .

ThomasJak 2 years ago

купить диплом в ангарске http://www.6landik-diploms.com

https://www.escaperoom.center 2 years ago

Hello! Do you know if they make any plugins to assist with Search Engine Optimization?

I’m trying to get my blog to rank for some targeted keywords but I’m not seeing very good gains.

If you know of any please share. Kudos! I saw similar blog here:

Good escape room

Kennethden 2 years ago

Kraken13.at вход – kraken darknet market, kraken ссылка тор

tiktok picture downloader 2 years ago

I needed to thank you for this good read!! I absolutely loved every little bit of it. I have got you book-marked to look at new stuff you post…

Russellliero 2 years ago

https://bi-cleaning.ru/

Alfredutemn 2 years ago

https://mclean.su/

StephenhEarT 2 years ago

купить диплом парикмахера https://6landik-diploms.com

Williammes 2 years ago

заказать такси онлайн https://taxi-novocherkassk.ru/

Henrypag 2 years ago

заказать такси приложение https://zakaz-taxionline.ru/

Rogerflump 2 years ago

Ищете способ расслабиться и получить незабываемые впечатления? Мы https://t.me/intim_tmn72 предлагаем эксклюзивные встречи с привлекательными и профессиональными компаньонками. Конфиденциальность, комфорт и безопасность гарантированы. Позвольте себе наслаждение и отдых в приятной компании.

Roberticers 2 years ago

Ищете способ расслабиться и получить незабываемые впечатления? Мы https://t.me/intim_tmn72 предлагаем эксклюзивные встречи с привлекательными и профессиональными компаньонками. Конфиденциальность, комфорт и безопасность гарантированы. Позвольте себе наслаждение и отдых в приятной компании.

EdwardShiem 2 years ago

https://faina-cleaning.ru/

MichaelErono 2 years ago

купить справку о болезни

Dennisvanna 2 years ago

Find Out More Fl studio download

FlanmeCiT 2 years ago

Проект перепланировки Москва alma-stroi.ru

Перепланировка квартиры — один из самых главных этапов в ремонте разных объектов. Но в нашей стране, она непременно должна быть законной и исполнена по всем правилам. Мы знаем о перепланировках всё, смотрите на сайте alma-stroi.ru прямо сейчас.

По теме услуги по узакониванию перепланировки мы поможем Вам. Если у Вас уже выполнена самовольная перепланировка без документов, то это не страшно. Её просто возможно узаконить и спокойно пользоваться зданием. Не всегда расположение комнат в квартире или промышленных помещениях удовлетворяет хозяина. Но в последнее время, перепланировка просто лучший выход из сложившейся ситуации. Конечно, выгоднее всего ее осуществлять на этапе начального ремонта, но если этого не случилось, то её возможно сделать на каждом этапе эксплуатирования.

Прайс на перепланировки можно посмотреть на интернет сайте alma-stroi.ru или увидеть примеры выполненных работ. Мы осуществляем работу в представленной теме уже множество лет и имеем множество счастливых клиентов и готовых работ. К каждому проекту имеем индивидуальный подход и учитываем все пожелания клиента. Также работаем четко в установленный срок и по очень приемлемым расценкам.

Заказать техническое заключение на перепланировку можно прямо сейчас. Наши специалисты приедут к Вам для замера комнат и определения размера работы. И после этого будет названа итоговая цена и дата выполнения работ. Перепланировка — это отличный шанс сделать свою жизнь комфортнее.

doramaserials.net 2 years ago

Корейские дорамы – это удивительный мир, который привлекает зрителей своими захватывающими сюжетами и невероятной актерской игрой. На сайте doramaserials.net вы можете смотреть корейские дорамы онлайн без рекламы и в высоком качестве. Удобный интерфейс и широкий выбор сериалов позволят вам легко найти то, что вы ищете. Погружайтесь в мир восточной романтики, драмы и комедии, наслаждаясь каждой минутой просмотра.

Сайт doramaserials.net – это идеальное место для тех, кто хочет наслаждаться корейскими дорамами онлайн без каких-либо помех. Высокое качество видео и отсутствие рекламы делают просмотр комфортным и приятным. Здесь каждый найдет сериал по своему вкусу, будь то захватывающий триллер или трогательная любовная история. Присоединяйтесь к миллионам поклонников корейских дорам и откройте для себя новые грани азиатского кинематографа на doramaserials.net.

DonaldCoale 2 years ago

эскорт мск – эскорт модели, эскорт модели москва

ArthurUrite 2 years ago

жк купить квартиру от застройщика купить квартиру в казани новостройка от застройщика

JosephNiz 2 years ago

onion сайты – теневой форум рутор, даркнет площадки

Williamres 2 years ago

купить квартиру в казани от застройщика https://kvartiru-kupit-kzn.ru

DanielFak 2 years ago

купить квартиру в казани от застройщика купить квартиру в казани новостройка от застройщика

Pillsvem 2 years ago

Erectile dysfunction treatments available online from TruePills.

Discreet, next day delivery and lowest price guarantee.

Viagra is a well-known, branded and common erectile dysfunction (ED) treatment for men.

It’s available through our Online TruePills service.

Trial ED Pack consists of the following ED drugs:

Viagra Active Ingredient: Sildenafil 100mg 5 pills

Cialis 20mg 5 pills

Levitra 20mg 5 pills

https://true-pill.top/

Nassa

Letus

Kardopal

Lerite

GeorgeJaw 2 years ago

атака титанов в хорошем качестве атака титанов смотреть онлайн

Robertocrick 2 years ago

волна darknet – volna даркнет маркет, волна даркнет ссылка

RobertVosus 2 years ago

navigate to this web-site The Sandbox Metaverse Map

ThomasExida 2 years ago

Find Out More What is the sandbox

GeorgeJaw 2 years ago

атака титанов онлайн атака титанов

GeorgePef 2 years ago

купить мебель

https://formomebel.ru/divany/modulnye

RonnieDuart 2 years ago

Meal options range from a hollanderhomes.com choice of hotels without services provided to full board.

RicardoRek 2 years ago

how to start an online casino gaming bets

Charlesrak 2 years ago

голяк смотреть онлайн в хорошем сериал голяк

DwightTop 2 years ago

голяк кубик в кубе смотреть https://golyak-serial-online.ru

Michaelrinna 2 years ago

форум вебкам моделей и моделей OnlyFans! Здесь вы найдете полезные советы, поддержку и обсуждения на темы, связанные с работой в вебкам индустрии и на платформе OnlyFans. Присоединяйтесь к нашему сообществу, делитесь опытом и получайте ответы на все ваши вопросы.

https://forum.vipcamclub.ru/

X22Nethy 2 years ago

Hey people!!!!!

Good mood and good luck to everyone!!!!!

GeorgeMew 2 years ago

see this The Sandbox Shop

AndrewNab 2 years ago

my link Notepad

aviator game zambia 2 years ago

and the player’s goal is to cash out before the plane crashes. This simple yet thrilling concept has made it a aviator game winning strategy

aviator game download apk 2 years ago

advancements have allowed for improved graphics, smoother gameplay, and more interactive features. These aviator game demo play

BrianPonge 2 years ago

The weight of the parcel ehappynews.com can be up to 20 kg, and its format must correspond to the size of the trunk.

Robert 2 years ago

Принимать финансовые решения может быть сложно. Но с нашим каталогом финансовых продуктов это стало проще, чем когда-либо!

оформить дебетовую карту

Мы собрали все лучшие финансовые продукты в одном месте, чтобы вы могли легко сравнить их и найти те, которые подходят именно вам. Наши экспертные обзоры и рейтинги помогут вам принять обоснованное решение, соответствующее вашим уникальным потребностям.

кредит банк

Независимо от того, ищете ли вы кредит наличными, дебетовую карту или инвестиционный счет, наш каталог финансовых продуктов поможет вам сделать правильный выбор.

Daniel 2 years ago

Ищете удобный способ сравнить и выбрать финансовые продукты? Загляните в наш каталог финансовых продуктов.

кредитные карты банков! У нас есть все, что вам нужно, от кредитов и дебетовых карт до сберегательных счетов и инвестиций.С нашим удобным поисковым инструментом вы можете быстро и легко найти продукты, соответствующие вашим конкретным потребностям.

займ взять А благодаря нашим подробным обзорам и сравнениям вы можете быть уверены, что принимаете обоснованное решение.Не тратьте время на утомительные поиски в Интернете.

кредит взять Посетите наш каталог финансовых продуктов сегодня и найдите идеальный продукт для ваших финансовых целей!

JamesAssog 2 years ago

нарколог лечение алкоголизма https://lechenie-narkomanii.kz/

SanchesLor 2 years ago

В Dragon money можно найти разнообразные азартные игры. Используйте промокоды vk.com/dragon_money_promokod для получения дополнительных выгод и бонусов. Каждый найдет здесь что-то по душе, включая самых опытных игроков. В этом сообществе я нашел множество бездепозитных промокодов.

octagon.express 2 years ago

Хотите быть в курсе всех свежих событий UFC? Octagon Express предлагает вам новости ЮФС на сегодня! Горячие интервью, детальные обзоры боев и последние новости ждут вас на нашем сайте. Не пропустите ни одной сенсации и будьте первыми, кто узнает все важные детали. Подписывайтесь на обновления и оставайтесь в курсе всех событий UFC вместе с Octagon Express!

octagon.express 2 years ago

Будьте всегда в курсе всех событий в мире Ultimate Fighting Championship вместе с Octagon Express! На нашем сайте вы найдете самые свежие новости UFC. Мы публикуем эксклюзивные интервью с бойцами, детальные обзоры боев и аналитические статьи от ведущих экспертов. Не пропустите ни одной важной новости и всегда оставайтесь в центре событий. Подписывайтесь на обновления и следите за всем, что происходит в мире UFC, с Octagon Express!

Gates_of_Olympu_ljkl 2 years ago

gates of olympus слот gates of olympus слот .

RussellSnomi 2 years ago

Портал о Ярославле – ваш гид по культурной жизни города. Здесь вы найдёте информацию о театрах, музеях, галереях и исторических достопримечательностях. Откройте для себя яркие события, фестивали и выставки, которые делают Ярославль культурной жемчужиной России.

Tommiechero 2 years ago

регистрация драгон мани казино драгон мани казино вход

aviator game bot 2 years ago

Cash Out: Decide when to cash out to secure your winnings. If you cash out before the plane crashes, you win. If aviator game bet

Felipeuseri 2 years ago

бонус 1go casino официальный сайт 1го казино

Josephteepe 2 years ago

1 квартира цена https://novostroyka-kzn16.ru

DanteGes 2 years ago

квартира от застройщика Санкт-Петербург https://kvartiru-kupit-spb.ru

SaburaJar 2 years ago

Питьева вода из скважин Иркутск мастер-буров.рф

Фирма Мастер Буров оказывает услуги по бурению скважин на Вашем участке в Иркутске и Иркутской области. Осуществляя работу в данной области уже множество лет, мы знаем все тонкости и предоставляем гарантию на свою работу в срок десять лет. А также, у нас работает рассрочка без процентов на 3 месяца, что очень удобно, если нет лишних денежных средств на данный момент. На сайте мастер-буров.рф ознакомьтесь с нашими ценами, примерами скважин и подобной интересной информацией.

По запросу бурение скважин в хомутово мы вам обязательно поможем. На данном онлайн ресурсе можно узнать примерную глубину бурения на своем участке в видео, а также цены. Но самый безупречный метод — это пригласить к себе мастера для выявления правильного места под скважину, определения объема работы и, в соответствии с этим, стоимость. Напишите контактный номер телефона и мы созвонимся с Вами в ближайшее время.

У нас личная техника с буровыми установками, которая предоставляет вероятность оказывать услуги высокого качества по очень приемлемым расценкам. В распоряжении 8 единиц техники и 22 эксперта с большим опытом. Вы также сможете приобрести всё самое нужное оборудование для водоснабжения. Это: химический анализ воды, набор для подключения, насос для скважины, гидроаккумулятор и другое. По любым вопросам позвоните по контактному телефону 8(3952)559-589 или приходите по адресу: г. Иркутск, мкр-н Радужный, д. 12, оф. 310.

Заказать скважину пробурить цена под ключ можно на сайте мастер-буров.рф прямо сейчас. Скважина с чистой водой — один из важных элементов на Вашем участке. Мы гарантируем качество работы, материалов, а также осуществляем сервисное обслуживание. Наружние факторы могут разрушительно влиять на скважину и качество воды, мы также работаем с восстановлением поврежденных скважин от поломок и с очисткой от заиливания. Звоните, приходите, будем рады с Вами сотрудничать.

DanaNethy 2 years ago

Slightly off topic 🙂

It so happened that my sister found an interesting man here, and recently got married ^_^

(Moderator, don’t troll!!!)

Is there are handsome people here! 😉 I’m Maria, 28 years old.

I work as a model, successfull – I hope you do too! Although, if you are very good in bed, then you are out of the queue!)))

By the way, there was no sex for a long time, it is very difficult to find a decent one…

And no! I am not a prostitute! I prefer harmonious, warm and reliable relationships. I cook deliciously and not only 😉 I have a degree in marketing.

My photo:

___

Added

The photo is broken, sorry(((

Check out my blog where you’ll find lots of hot information about me:

https://grushacafe.ru

Or write to me in telegram @Lolla_sm1_best ( start chat with your photo!!!)

Timsothylem 2 years ago

Excellent post. Keep posting such kind of information on your page. Im really impressed by your site.

Hi there, You’ve performed an excellent job. I’ll certainly digg it and personally recommend to my friends. I’m confident they’ll be benefited from this web site.

купить диплом в ангарске

http://seo1st.ru

http://maksimdovzhenko.ru

http://irkutsk-arbitr.ru

купить диплом с внесением в реестр

BillySit 2 years ago

ozempic buy – меню +для похудения, аземпик фото

Antoniodeari 2 years ago

российский оземпик – недорогие препараты +для похудения, семаглутид цена +в аптеке

Brandontet 2 years ago

cialis online pharmacy australia : viagra cznadian pharmacy online pharmacy reviews https://mexicopharmacy.top

aviator predictor tips and tricks 2 years ago

become more comfortable with the gameplay. Observing patterns and understanding the timing of the plane’s ascent best way to play aviator

youtube to mp3 converter safe 2024 2 years ago

I absolutely love your website.. Very nice colors & theme. Did you develop this web site yourself? Please reply back as I’m wanting to create my own personal site and would like to find out where you got this from or just what the theme is named. Cheers.

JoaquinNache 2 years ago

квартиры в новостройках Санкт-Петербурге https://novostroyki-spb78.ru

aviator demo game play 2 years ago

Advanced Tips for Experienced Players aviator casino game demo

Проститутки ДНР 2 years ago

Если вы хотите заказать проститутку онлайн, заходите на сайт intimdnr.com – элитные проститутки . Мы предлагаем вам удобный сервис и широкий выбор проверенных девушек. Каждая анкета тщательно проверена, чтобы гарантировать вам безопасность и высокий уровень обслуживания. Наши девушки красивы, умны и профессиональны, что делает каждую встречу незабываемой. Выбирайте понравившуюся девушку и оставляйте заявку на сайте. На intimdnr.com – проститутки города с выездом вы найдете всё, чтобы ваша встреча прошла на высшем уровне. Закажите проститутку онлайн и наслаждайтесь приятным времяпрепровождением с идеальной спутницей.

Brianecorp 2 years ago

Каталог эротических рассказов https://vicmin.ru подарит тебе возможность уйти от рутины и погрузиться в мир секса и безудержного наслаждения. Обширная коллекция рассказов для взрослых разбудит твое воображение и принесет немыслимое удовольствие.

MichaelStags 2 years ago

обменять биткоин на рубли – купить btc, обменять биткоин

Efremldom 2 years ago

На сайте https://3d-printery-77.ru/ в огромном выборе находятся 3D принтеры, которые идеально подходят для выполнения самых разных задач. Вы всегда сможете воспользоваться профессиональной консультацией, а на всю продукцию предоставляется гарантия качества. Организуется оперативная доставка по стране. Все принтеры представлены именитыми, проверенными и надежными брендами, которые дорожат репутацией. Также есть изделия, которые предназначены для профессионального использования.

aviator game free demo 2 years ago

Ensuring Safe Gaming Practices aviator game formula

Alfredaxova 2 years ago

Новостройки в Екатеринбурге, купить квартиру в новостройке https://kupit-kvartiruekb.ru от застройщика. Строительство жилой и коммерческой недвижимости. Высокое качество, прозрачность на всех этапах строительства и сделки.

MichaelTub 2 years ago

купить диплом об образовании https://diplom-izhevsk.ru

비아그라 구매 2 years ago

비아그라 구매 사기 방지하는 방법 불행히도, 온라인 세계는 의심하지 않는 구매자를 대상으로 하는 사기로 가득 차 있습니다. 다음은 온라인에서 비아그라를 사는 것과 관련된 몇 가지 일반적인 사기 및 이를 피하는 방법입니다

Keithvaddy 2 years ago

Cериал Голяк https://golyak-serial-online.ru смотреть онлайн в хорошем качестве и с лучшей озвучкой на любых устройствах. Все сезоны истории мелкого преступника Винни и его друзей в английском городке!

PerryTiepe 2 years ago

Excellent and high-quality Crystal-Watson, рџ’— nude on live sex chat absolutely free and easy to watch on any device, just

Nude hot cams girlNaked amateur webca fcc0886

StanleyVub 2 years ago

Драгон Мани Казино https://krpb.ru – ваше место для азартных приключений! Наслаждайтесь широким выбором игр, щедрыми бонусами и захватывающими турнирами. Безопасность и честная игра гарантированы. Присоединяйтесь к нам и испытайте удачу в самом захватывающем онлайн-казино!

pin up aviator 2 years ago

History and Development 1win aviator

Davidicoth 2 years ago

Famous French footballer Kylian Mbappe https://kylianmbappe.prostoprosport-ar.com has become a global ambassador for Dior. The athlete will represent the men’s collections of creative director Kim Jones and the Sauvage fragrance, writes WWD. Mbappe’s appointment follows on from the start of the fashion house’s collaboration with the Paris Saint-Germain football club. Previously, Jones created a uniform for the team where Kylian is a player.

Мастер-Буров 2 years ago

Относительно бурение скважин на воду цена мы вам непременно окажем помощь. На представленном веб ресурсе можно узнать примерную глубину бурения на своем участке в видео, а также цены. Но самый безошибочный способ — это позвать к себе специалиста для выявления правильного участка под скважину, понятие объема работы и, в соответствии с этим, прайс. Оставьте контактный номер телефона и мы созвонимся с Вами в скорое время.

online 2 years ago

buy generic viagra in us

application aviator predictor 2 years ago

Playing the Aviator Game is a thrilling experience. Players place their bets and watch the plane take off, with aviator app predictor login

crazymonkey_rrMi 2 years ago

играть crazy monkey https://www.crazy-monkey-ru.ru .

pharmacy 2 years ago

bactrim 160

aviator game fraud 2 years ago

game is random and unbiased, providing a fair chance for all players to win. aviator game fake or real

RebeccaVew 2 years ago

ENG

Crossfit bot is an exciting clicker game in which you have the opportunity to earn normal money for free. Control your bot by clicking on the screen and collecting coins to improve its skills and capabilities. Immerse yourself in the exciting world of http://cross-finance.tilda.ws/ and compete with other players for the first place in the ranking! Check out the http://cross-finance.tilda.ws/

RUS

Crossfi bot – это захватывающая игра-кликер, в которой вы имеете возможность заработать нормальные деньги совершенно бесплатно. Управляйте своим ботом, кликая по экрану и собирая монеты для улучшения его навыков и возможностей. Погрузитесь в захватывающий мир http://cross-finance.tilda.ws/ и соревнуйтесь с другими игроками за первое место в рейтинге! Ознакомьтесь на http://cross-finance.tilda.ws/

http://cross-finance.tilda.ws/

order 2 years ago

where to buy azithromycin online

RobertPaype 2 years ago

моунжаро купить – mounjaro отзывы, тирзепатид инструкция цена

Joshuagew 2 years ago

Скачать свежие новинки песен https://muzfo.net 2024 года ежедневно. Наслаждайтесь комфортным прослушиванием, скачивайте музыку за пару кликов на сайте.

Jeffreydut 2 years ago

הנימוסים המקסימים שלהן והגוף המושלם מרגשים גברים שיוצאים עם הפצצות. בחרו את הבחורה המושלמת שלכם כל הגברים שצריכים עיסוי אירוטי גברים ולהפתיע אותם עם כישורים ופינוק מעולה. אחרי דייט אחד עם בחורה כזאת, לעולם לא תפסיקו לחלום על לחזור לאטמוספירה הזאת. ההנאה נערות ליווי ברמת גן

Dominiclok 2 years ago

allnews-24.com

LhaneNamma 2 years ago

It’s amazing for me to have a site, which is beneficial designed for my knowledge. thanks admin

купить диплом в рубцовске

http://cardioevent.ru

http://publicspaces17.ru

http://borovskie-izvestiya.ru

купить диплом строителя

Stephenetews 2 years ago

Всем привет! Подскажите, где найтиполезные статьи о недвижимости? Сейчас читаю https://amistar-lak.ru

CharlesRak 2 years ago

Wide variety of designs and styles home365.net. An environmentally friendly material that does not produce toxic emissions and does not contain formaldehyde, unlike plastic analogues.

jogar aviator online grГЎtis 2 years ago

Convenience: Play from the comfort of your home or on the go. aviator game 1 win

WilliamCes 2 years ago

Скачать свежие новинки песен https://muzfo.net 2024 года ежедневно. Наслаждайтесь комфортным прослушиванием, скачивайте музыку за пару кликов на сайте.

JasonRoP 2 years ago

mounjaro tirzepatide цена – мунджаро фото, тирзепатид москва

order 2 years ago

doxycycline 400 mg

cheap 2 years ago

prednisone 20mg tablets

how to beat the aviator game 2 years ago

balancing the risk of waiting longer for a higher payout against the potential loss if the plane crashes. how to win aviator game

Jamesdache 2 years ago

Агентство по продвижению телеграм-каналов https://883666b.com в Москве специализируется на разработке и реализации стратегий для увеличения аудитории и вовлечённости подписчиков на телеграм-каналах. Эксперты агентства помогают клиентам определить целевую аудиторию, разрабатывают контент-планы и рекламные кампании. Услуги включают рекламу посевами, таргет рекламой, анализ конкурентов, SEO-оптимизацию контента.

CharlesSkach 2 years ago

интернет эквайринг https://internet-ekvajring.kz – безопасные и эффективные платежные решения для вашего бизнеса.

drugs 2 years ago

clomid purchase online

Timsothylem 2 years ago

Приветики!

На нашем сайте вы можете выбрать и приобрести диплом Вуза с гарантией и доставкой в любой регион России по самым низким ценам.

http://www.devils-rock.at/index.php?option=com_easybookreloaded

https://ssa.ru/forum/kupit-diplom-vasha-dver-k-luchshemu-buduschemu-i-uspeshnoi-karere.html

http://chl-fomin.blogspot.com/2016/06/mac-os-x-installation.html

https://www.ntwk.ru/forum/index.php?/forum/14-%D1%84%D0%BB%D0%B5%D0%B9%D0%BC/&do=add

http://test.kuli4kam.net/gallery/image/224-%D0%B4%D0%B8%D0%BF%D0%BB%D0%BE%D0%BC%D1%8B-%D0%BD%D0%B0-%D0%B1%D0%BB%D0%B0%D0%BD%D0%BA%D0%B5-%D0%B3%D0%BE%D0%B7%D0%BD%D0%B0%D0%BA-%D0%BF%D1%80%D0%B8%D0%BE%D0%B1%D1%80%D0%B5%D1%82%D0%B0%D0%B9-%D0%BE%D0%BD%D0%BB%D0%B0%D0%B9%D0%BD/

OLaneNamma 2 years ago

I got this web page from my pal who told me about this site and now this time I am visiting this site and reading very informative articles at this place.

http://evolutionist.ru/словарь-терминов-и-понятий-трансерфи/

купить диплом во всеволожске

http://lk3-eng.ru

купить диплом в азове

EddieBok 2 years ago

http://pbxhit.com

http://defloration.tv

eporner.com

CASINO XSS DRUGS

C4 КАЗИНО HEROINE

Этот сайт тоже не очень

https://otzovik.com/reviews/kompaniya_bayer/

Если порно то то только лучшее тут

https://porno666.link

https://seg.batsa.pro

https://king-vulkan.casino/

https://rt.pornhub.com/

xhamster.com франшиза bigdata отзывы

C4 КАЗИНО HEROINE

https://epicafri.com

http://adm-komsomolsk.ru/

xnxx.com

eporner.com

Партнёрская программа 1persuade интернациональной букмекерской компании. Работают на беттинг а также гемблинг вертикалях. Платят до 60% по RevShare, индивидуальные условия по CPA также Cross моделям

http://www.defloration.tv (https://www.defloration.tv)

Caseynub 2 years ago

Откройте для себя мир турецких сериалов на русском языке на сайте turkvideo.tv. Здесь вы найдете широкий выбор захватывающих сюжетов и популярных актеров, доступных для просмотра в отличном качестве. Посетите раздел турецкие сериалы на русском языке, чтобы наслаждаться любимыми сериалами без необходимости искать переводы. Этот сайт идеально подходит для всех любителей турецкого кинематографа, предлагая удобный доступ к лучшим сериалам Турции с русской озвучкой. Присоединяйтесь и начните смотреть уже сегодня!

WilliamSkync 2 years ago

оземпик купить +в минске – оземпик препарат отзывы инструкция +по применению, саксенда екатеринбург

aviator slot 2 years ago

increase the excitement of the game. aviator prediction

price 2 years ago

dexamethasone 4 mg price

EddieNut 2 years ago

עילית והסביבה הקרובה דירות דיסקרטיות אליהן מגיעים גברים ונשים לבילויים דיסקרטיים תוכלו למצוא בכל רחבי הארץ וגם בנצרת. אלו הן צעצועי עיסוי עבור משחקי תפקידים, יש הרבה אביזרים בבית שלהן. לכן, הן מוכנות ליחס דומה מהגברים. בנות בשירותי עיסויים צריכות דברים סקס אדיר דירות דיסקרטיות

aviator apk predictor 2 years ago

advancements have allowed for improved graphics, smoother gameplay, and more interactive features. These aviator apk for pc

purchase 2 years ago

medication amoxicillin 500mg

RalphWaync 2 years ago

Kraken13.at сайт – kraken ссылка зеркало официальный, kraken darknet ссылка

sale 2 years ago

accutane price

aviator casino en ligne 2 years ago

Playing the Aviator Game online offers several benefits: aviator casino online

Patrickfravy 2 years ago

купить квартиру от застройщика купить квартиру в казани от застройщика

Patrickfravy 2 years ago

жк купить квартиру от застройщика https://nedvizhimost47.ru

Charlessip 2 years ago

Законодательно закреплено положение о том, что если организация (ИП) в течение года изменила место нахождения (место жительства), то налог (авансовые платежи по налогу) исчисляются по налоговой ставке, которая установлена законом субъекта РФ по новому месту нахождения организации (месту жительства ИП) https://kalm-invest.ru/privacy-policy

Ранее такой порядок в НК РФ не был закреплен, но его рекомендовали контролирующие ведомства (см https://kalm-invest.ru/privacy-policy

, например, письмо Минфина России от 23 https://kalm-invest.ru/

05 https://kalm-invest.ru/privacy-policy

2023 № 03-11-09/46940, доведенное до сведения налоговых органов письмом ФНС России от 09 https://kalm-invest.ru/buhu4et

06 https://kalm-invest.ru/buhu4et

2023 № СД-4-3/7372@, см https://kalm-invest.ru/privacy-policy

статью-рекомендацию) https://kalm-invest.ru/

Эта поправка вступит в силу с 01 https://kalm-invest.ru/services

01 https://kalm-invest.ru/privacy-policy

2024 https://kalm-invest.ru/privacy-policy

поквартальном уменьшении с заявлением о зачете, если будет платить фиксированные взносы по такому графику:

Помогла статья? Получите еще секретный бонус и полный доступ к справочной системе БухЭксперт8 на 14 дней бесплатно https://kalm-invest.ru/

Объект

Для зачета нужно, чтобы :

ИП может уменьшить налог на суммы страховых взносов, уплаченных за себя и за своих сотрудников https://kalm-invest.ru/buhu4et

LewisReabs 2 years ago

Hi! Do you use Twitter? I’d like to follow you if that would be ok. I’m absolutely enjoying your blog and look forward to new updates.

купить диплом историка

http://magistratura-svfu.ru

http://naykadokcinema.ru

http://sprchita.ru

купить диплом в кисловодске

Charlesreolf 2 years ago

Все наши межкомнатные двери можно собрать в блок и врезать фурнитуру на производстве, выбрать вариант заполнения, изготовить под Ваш проем индивидуально, изготовить как противопожарные EI30 и звукоизоляционные, сроки минимальные! Звоните по телефону 8 (495) 722-62-28 (Москва и Московская область) или 8 (800) 200-61-33 (по России, бесплатно) https://www.dvervam.ru/catalog/razobrat-dev/interior-doors/sodruzhestvo/s-8-cagrovie/

Для внутреннего наполнения полотна используем брус хвойной древесины, тогда как другие изготовители применяют МДФ https://www.dvervam.ru/catalog/razobrat-dev/metallicheskie-dveri/labirint/dobory-i-nalichniki/?sort=active_from&direction=desc

Цельное дерево значительно увеличивает срок службы дверей https://www.dvervam.ru/catalog/razobrat-dev/morelli-ru/filter/clear/apply/?sort=name&direction=desc

Каркас полотна изготавливаем из сосны https://www.dvervam.ru/catalog/mezhkomnatnye-dveri2/dveri-albero1/

Свойства этого материала исключают перекос дверей со временем, разбухание или усыхание http://www.dvervam.ru/news/?sort=NAME&direction=desc

Делаем фабричную врезку под замок и петли http://www.dvervam.ru/catalog/mezhkomnatnye-dveri2/filter/clear/apply/?sort=catalog_PRICE_1&direction=desc

Это позволяет избежать образования мусора и пыли во время монтажа и сокращает время установки дверей https://www.dvervam.ru/catalog/razobrat-dev/velldoris-net/mezhkomnatnye-dveri-polotna/dvernoe-polotno-emal-scandi-neo-7-glukhoe-2p-800kh2000-tsvet-belyy/

Пластиковые двери CPL или HPL — более 300 вариантов отделки износостойким, влагостойким пластиком высокого давления производства — Arcobolena, Egger или Slotex http://www.dvervam.ru/catalog/mezhkomnatnye-dveri2/dveri-albero1/mezhkomnatnaya-dver-albero-singapur-5-eko-shpon/

Полностью имитирующим текстуру дерева, шпона и даже мрамора, подойдут под любой дизайн-проект https://www.dvervam.ru/catalog/vkhodnye-dveri1/dveri-imperiya/mezhkomnatnaya-dver-triumf/

2250х760х200 2250х860х200 https://www.dvervam.ru/catalog/razobrat-dev/metallicheskie-dveri/filter/clear/apply/?sort=name&direction=asc

550х1900 600х1900 600х2000 700х2000 800х2000 900х2000 950х2100 950х2200 https://www.dvervam.ru/catalog/mezhkomnatnye-dveri2/dveri-vfd/mezhkomnatnaya-dver-bp-doors-sheyl-dors-tetra-8/

Stevenquing 2 years ago

Толщиномер поможет без эксперта определить не только место покраски, но и серьезность дефекта определенной детали кузова https://www.ndt-club.com/product-867-komplekti-znakov-markirovochnih.htm

Прибор недорогой и несложный в эксплуатации https://www.ndt-club.com/product-510-volna-yf365-portativnii-yltrafioletovii-fonar-s-fokysiryushei-linzoi.htm

Но при этом необходимо учитывать некоторые особенности, чтобы получить более точные показания https://www.ndt-club.com/product-483-indykcionnii-nagrevatel-easytherm-100-hq.htm

Портативный высокоточный многофункциональный ультразвуковой толщиномер TT310 (комплект) предназначен для измерения толщины различных изделий путем сканирования изделия при помощи ультразвука

Наш сайт, специализирующийся на измерителях ЛКП, обладает удобным интерфейсом, возможностью обратной связи для помощи вам и широким ассортиментом https://www.ndt-club.com/product-191-tvr-am-mehanicheskii-shtativ-s-tverdomerom-durometrom-tvr-a.htm

Выбирать у нас интересно и удобно, а покупать – безопасно, легко, быстро и приятно!”

ThomasAnalm 2 years ago

Когда все нужные доски и прочие материалы будут готовы, производятся следующие работы https://kpdkamen.ru/contacts/

Выбор фартука мы начали с изучения информации в интернете: смотрели обзоры на разные виды столешниц https://kpdkamen.ru/articles/sovremennye-lestnitsy-iz-kamnya-dlya-zagorodnyh-domov/

Вскоре мы узнали, что кроме плитки есть много вариантов оформления: стекло, дерево, камень https://kpdkamen.ru/portals/

Но бывают и бесшовные варианты оформления плиткой https://kpdkamen.ru/articles/granit-kak-oblitsovochnyj-material/

Подобрать материал можно под любой бюджет — от недорогих коллекций отечественных производителей по 400 Р за 1 м? до эксклюзивных итальянских коллекций, стоимость которых исчисляется сотнями тысяч рублей за 1 м? https://kpdkamen.ru/articles/statya1/

Дерево https://kpdkamen.ru/portals/

Экологичный, приятный и https://kpdkamen.ru/actions/offer-sale/